ITC Reversal Under Rule 37:

The 180-Day Rule & Practical Difficulties

What triggers the reversal, how interest bites, when you can re-claim — and the real-world scenarios where Rule 37 creates compliance headaches.

- Part 1 — What is Input Tax Credit? A Plain-English Guide

- Part 2 — Section 16: Conditions for Claiming ITC

- Part 3 — Blocked Credits under Section 17(5)

- Part 4 — Interest under Section 50 of the CGST Act

- Part 5 — ITC on Capital Goods

- ▶ Part 6 — ITC Reversal under Rule 37 (You are here)

- Part 7 — Input Service Distributors (ISD) under GST

📌 At a Glance

- Rule 37 implements the proviso to Section 16(2)(b) — if the supplier is not paid within 180 days of the invoice date, ITC must be reversed.

- Reversal is required in the GSTR-3B of the month in which the 180th day falls, filed through the GST portal.

- Interest at 18% p.a. under Section 50(1) applies from the date ITC was claimed to the date of reversal.

- On subsequent payment to the supplier, the ITC can be re-claimed in the period of payment.

- Rule 37A introduces a parallel track — reversal when the supplier has not filed GSTR-3B, regardless of buyer’s own payment.

- Practical difficulties include tracking deadlines across hundreds of invoices, disputed payments, credit notes, partial payments, and barter/non-monetary consideration.

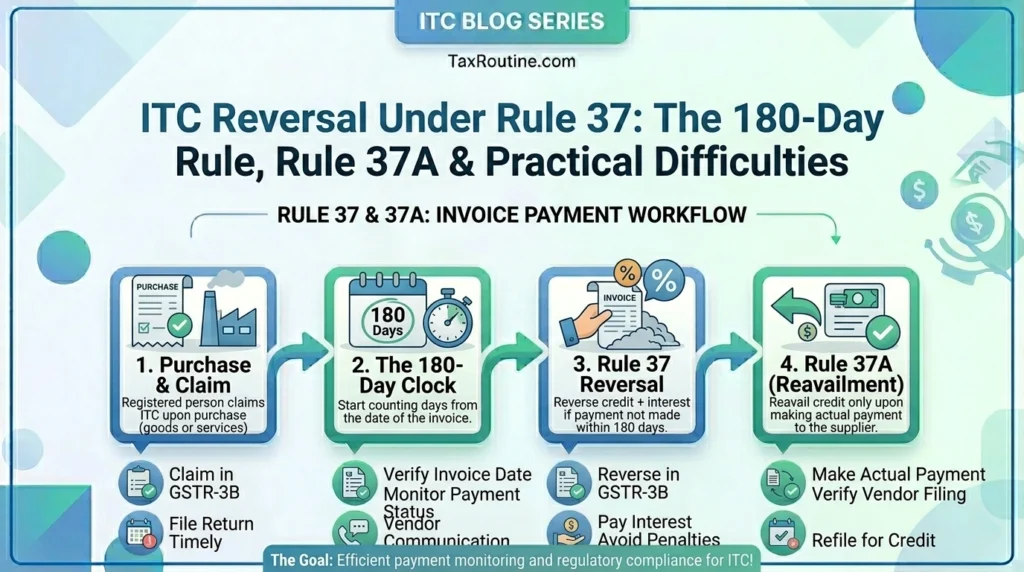

1. Statutory Basis: Section 16(2)(b) & Rule 37

The 180-day rule has its roots in the proviso to Section 16(2)(b) of the CGST Act. The proviso states that where a registered person fails to pay the supplier the amount towards the value of supply along with the tax payable thereon within 180 days from the date of issue of the invoice, an amount equal to the ITC availed shall be added to the output tax liability — along with interest under Section 50.

Rule 37 of the CGST Rules, 2017 operationalises this proviso. It prescribes when the reversal must be made, how to calculate the proportionate reversal for partially-paid invoices, and how the re-credit works once payment is eventually made.

The 180-day rule exists to prevent ITC from becoming a tool for leveraging unpaid credit. Without this rule, a buyer could claim full ITC on an invoice and then indefinitely delay paying the supplier — effectively getting a free float on the tax credit at the government’s expense. The rule ensures that ITC is tied to the underlying commercial transaction being genuinely completed. Read the full text of Section 16 on CBIC.gov.in →

2. How Rule 37 Works: Step by Step

3. Computation: Full vs Partial Payment

Rule 37 addresses both full non-payment and partial payment situations. Where only a portion of the invoice is paid within 180 days, the reversal is proportionate to the unpaid amount.

Where the registered person has paid only a part of the invoice value, the ITC to be reversed is computed as:

ITC Reversal = (ITC on invoice) × (Unpaid value ÷ Total invoice value)

Read the full text of Rule 37 in the CGST Rules →

Buyer pays 60% of an invoice but the remaining 40% is outstanding at Day 181

Invoice value: ₹10,00,000 + GST at 18% = ₹1,80,000. Total payable: ₹11,80,000.

ITC claimed: ₹1,80,000 (in Month 1 GSTR-3B).

Amount paid within 180 days: ₹7,08,000 (60% of ₹11,80,000).

Amount unpaid at Day 181: ₹4,72,000 (40% of ₹11,80,000).

ITC to reverse: ₹1,80,000 × 40% = ₹72,000

Interest at 18% p.a. on ₹72,000 from date of ITC claim to date of reversal (say 6 months): ₹72,000 × 18% × 6/12 = ₹6,480

ITC retained (on paid portion): ₹1,08,000 — no reversal required on this.

When the remaining ₹4,72,000 is eventually paid, ₹72,000 ITC can be re-claimed in that month’s GSTR-3B.

4. Rule 37A: Supplier Non-Filing — A Parallel Track

Rule 37A was introduced by CBIC Notification No. 26/2022-CT to address a different but related problem — what happens when the supplier does not file GSTR-3B, even though the buyer has already paid the supplier?

Under Rule 37A, if the supplier has filed GSTR-1 (invoice visible in GSTR-2B on the GST portal) but has not filed GSTR-3B for the relevant period, the buyer must reverse the ITC if the supplier’s GSTR-3B remains unfiled by 30th September of the financial year following the year of the invoice.

| Parameter | Rule 37 (Buyer Non-Payment) | Rule 37A (Supplier Non-Filing) |

|---|---|---|

| Trigger | Buyer has not paid supplier within 180 days | Supplier has filed GSTR-1 but not GSTR-3B |

| Deadline for reversal | GSTR-3B for the month in which Day 181 falls | GSTR-3B for the month of September of the FY following the invoice FY |

| Interest rate | 18% p.a. under Section 50(1) | 18% p.a. under Section 50(1) |

| Re-claim possible? | Yes — on payment to supplier | Yes — once supplier files GSTR-3B and pays tax |

| Buyer’s control | Full — buyer can pay supplier to avoid reversal | None — buyer cannot force supplier to file return |

Rule 37A places a significant compliance burden on innocent buyers. A buyer who has paid their supplier in full and claimed ITC correctly can still be forced to reverse that ITC — and pay 18% interest under Section 50(1) — simply because their supplier failed to file a return. The only remedy is to pursue the supplier to file, or absorb the cost and re-claim once the supplier eventually files.

5. Practical Difficulties Under Rule 37

Rule 37 is straightforward in concept but operationally demanding. Below are the most common real-world challenges businesses and their CAs face when navigating GST compliance under this rule.

Tracking 180-Day Deadlines Across Hundreds of Invoices

Payment Withheld Due to Defective Goods or Commercial Disputes

Partial Payments and Multiple Tranches Against Single Invoices

Credit Notes Received After ITC Is Claimed

Non-Monetary Consideration / Barter Transactions

Supplier Goes Insolvent or Untraceable Before Payment

Determining Whether “Payment” Includes TDS / TCS Deducted

6. Interest on Rule 37 Reversal: Recap

As covered in detail in Part 4 of this series, Rule 37 reversals attract interest at 18% p.a. under Section 50(1) — not 24%. This is because the reversal is treated as a delayed discharge of tax liability rather than a wrongful ITC claim.

| Event | Interest Rate | Interest Period |

|---|---|---|

| Rule 37 reversal (buyer non-payment beyond 180 days) | 18% p.a. | From date ITC was originally availed to date of reversal in GSTR-3B |

| Rule 37A reversal (supplier non-filing) | 18% p.a. | From date ITC was originally availed to date of reversal |

| ITC re-claimed after reversal (post payment / post supplier filing) | Nil | No fresh interest on re-credited ITC |

| Interest already paid on reversal period | Not refundable | The interest cost of the delay is a sunk cost even after re-claim |

If you know a payment will not be made within 180 days, consider reversing the ITC proactively before Day 181. This reduces the interest period and demonstrates voluntary compliance. The ITC can still be re-claimed once payment is made, with no interest on the re-credit.

7. How to Report Rule 37 Reversals in GSTR-3B

| Table in GSTR-3B | What to Enter |

|---|---|

| Table 4(B)(1) | ITC reversed as per Rule 42 & 43 — for capital goods mixed use (not Rule 37) |

| Table 4(B)(2) | ITC reversed on account of Rule 37 (non-payment to supplier within 180 days) and Rule 37A (supplier non-filing) — report the reversal amount here |

| Table 4(A)(5) | When re-claiming ITC after payment to supplier post-reversal — enter re-claim in the “All other ITC” row of Table 4(A) |

| Table 5.1 | Interest payable on the reversal — computed separately and paid in cash through the electronic cash ledger on gst.gov.in |

Many businesses mistakenly report Rule 37 reversals in Table 4(B)(1) — which is meant for Rule 42/43 proportionate reversals — instead of Table 4(B)(2). While the net effect on ITC is the same, incorrect table allocation can lead to discrepancies in GSTR-9 reconciliation and trigger scrutiny queries. Always use Table 4(B)(2) specifically for Rule 37 and Rule 37A reversals.

8. Quick Reference: Rule 37 & Rule 37A at a Glance

| Parameter | Position Under Rule 37 / Rule 37A |

|---|---|

| Statutory basis | Proviso to Section 16(2)(b) → Rule 37; Rule 37A (Notification 26/2022-CT) |

| Rule 37 trigger | Non-payment of invoice value (value + GST) to supplier within 180 days of invoice date |

| Rule 37A trigger | Supplier files GSTR-1 but not GSTR-3B by 30th September of following FY |

| Reversal deadline — Rule 37 | GSTR-3B for the month in which the 181st day falls |

| Reversal deadline — Rule 37A | GSTR-3B for October (due 20th November) of the following FY |

| Partial payment | Proportionate reversal — ITC × (unpaid value ÷ total invoice value) |

| Interest rate | 18% p.a. under Section 50(1) — from date of ITC claim to date of reversal |

| Interest payment mode | Cash only — electronic cash ledger via gst.gov.in; ITC cannot be used |

| Re-claim of ITC | Yes — in GSTR-3B of the month payment is made (Rule 37) or supplier files GSTR-3B (Rule 37A) |

| GSTR-3B table for reversal | Table 4(B)(2) |

| GSTR-3B table for re-claim | Table 4(A)(5) — All other ITC |

Frequently Asked Questions

- Part 1 — What is Input Tax Credit? A Plain-English Guide

- Part 2 — Section 16: Conditions for Claiming ITC

- Part 3 — Blocked Credits under Section 17(5)

- Part 4 — Interest under Section 50 of the CGST Act

- Part 5 — ITC on Capital Goods

- ▶ Part 6 — ITC Reversal under Rule 37 (You are here)

- Part 7 — Input Service Distributors (ISD) under GST